FREE CREDIT SCORE

BEST INTEREST RATES

FREE CREDIT SCORE

BEST INTEREST RATES

Buying a house usually involves taking a long-term loan, often lasting 20 to 30 years. Because of this long tenure, the interest rate on your loan plays a crucial role in deciding how much you ultimately pay for your home.

Even a small difference in home loan interest rates can create a major impact on your finances. For instance, if the interest rate on a ₹50 lakh loan changes by just 0.5%, the total interest paid over the loan tenure can increase or decrease by several lakhs.

In 2026, lenders across India are competing aggressively to attract borrowers. Many banks and housing finance companies are offering house loan interest rates starting around 7.1%–7.25%, though the final rate depends on your financial profile.

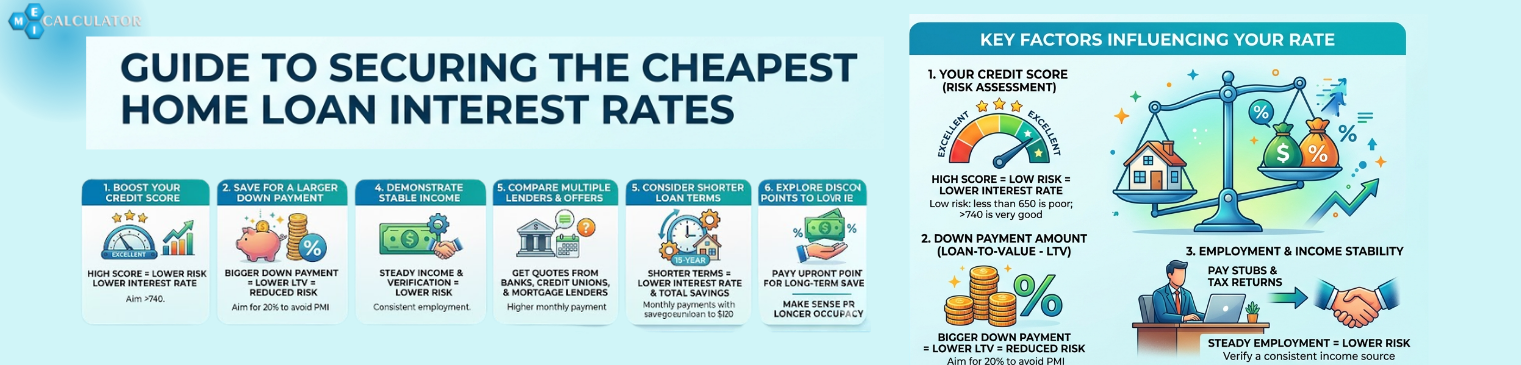

If you want to secure the cheapest interest rate home loan, preparation matters. Borrowers who understand how lenders evaluate applications and plan their loan structure carefully can often get significantly better rates.

Below are some practical ways to increase your chances of getting the lowest housing loan interest rate in India.

Two people applying for the same loan amount may receive completely different interest rates. This happens because lenders evaluate risk before approving a loan.

In India, most floating home loan interest rates are linked to benchmark rates such as the repo rate set by the Reserve Bank of India. However, the final rate offered to each borrower depends on their financial strength.

Key factors that influence house loan interest rates include:

Because of these variables, lenders may offer different lowest interest home loan options to different borrowers.

Your credit score is one of the most important elements lenders examine when deciding home loan interest rates.

In India, lenders typically rely on scores provided by TransUnion CIBIL. A high score signals that you manage credit responsibly and are less likely to default.

General credit score impact:

CIBIL Score | Expected Interest Rate Impact |

800+ | Access to cheapest interest rate home loan |

750–799 | Competitive rates |

700–749 | Slightly higher rates |

Below 700 | Higher risk pricing |

Improving your credit score before you apply home loan can lead to significant savings over time.

Many borrowers simply apply with the bank where they hold their savings account. While convenient, this approach may not always give you the best home loan interest rates.

Different lenders price loans differently based on their lending strategy. Some banks focus on aggressive home loan growth and may offer lower rates to attract borrowers.

To identify the cheapest interest rate home loan, it is wise to compare offers from:

Even a small difference in house loan interest rates can significantly change your EMI and overall repayment amount.

Your contribution towards the property price can influence the interest rate offered by lenders.

When borrowers pay a larger upfront amount, the loan amount reduces. This lowers the lender’s risk and often results in better pricing.

Typical impact of down payment:

Loan Tenure | Interest Rate Trend |

10–15 years | Lower rates |

20 years | Moderate rates |

25–30 years | Slightly higher rates |

A higher down payment can also reduce your EMI burden, which makes loan repayment easier.

Loan tenure directly affects both your EMI and the interest rate offered.

Longer loan tenures lower monthly EMIs but usually result in higher total interest payments. Some lenders also charge slightly higher house loan interest rates for very long repayment periods.

For example:

Down Payment | Loan Risk | Interest Rate |

10–15% | Higher risk | Higher rate |

20–25% | Moderate risk | Competitive rate |

30%+ | Low risk | Cheapest interest rate home loan |

Before finalising the tenure, many borrowers use an EMI calculator to see how different tenures affect their repayment schedule.

Adding a co-applicant can strengthen your loan application.

Banks evaluate the combined financial strength of both applicants, which can improve your eligibility and reduce perceived lending risk.

A co-applicant can help if they have:

This strategy can increase your chances of receiving the lowest interest home loan rate.

Home loans in India are usually available in two forms: fixed rates and floating rates.

Most borrowers choose floating home loan interest rates because they generally start lower and move with changes in the benchmark rates set by the Reserve Bank of India.

When interest rates decline in the economy, floating-rate borrowers may benefit through:

Fixed-rate loans, on the other hand, are usually priced higher because lenders factor in future uncertainty.

Many borrowers assume interest rates are fixed once quoted, but lenders often have flexibility.

If you have a strong financial profile and receive competing offers, you may be able to negotiate a lower rate.

Borrowers with excellent credit scores sometimes reduce their lowest housing loan interest rate by 0.10% to 0.30% through negotiation.

Banks and housing finance companies frequently provide small interest concessions for certain borrowers.

Common offers include:

These benefits may look small initially, but can reduce the total interest payable over the life of the loan.

The home loan market in India continues to remain competitive in 2026. Many lenders are offering house loan interest rates starting around 7.10%–7.25%, depending on the borrower’s profile and the loan structure.

Because interest rates can change when benchmark rates move, borrowers should evaluate different scenarios before finalising a loan.

Using an EMI calculator helps you estimate:

This allows borrowers to make more informed financial decisions before applying.

Securing the cheapest interest rate home loan requires more than choosing a bank with the lowest advertised rate. Your credit profile, loan structure, and negotiation strategy all play an important role.

To improve your chances of getting the best home loan interest rates, remember to:

Before finalising your loan, it is always helpful to calculate your EMI to understand how interest rates and tenure affect your repayment. This simple step can help you plan your finances better and choose the most affordable home loan option.

11 Comments

📆 Transfer to you. GET >>> graph.org/BALANCE-36824-US-DOLLARS-04-24?hs=951d4c11dce981b07702e39fca84b60e&

63e0uo

📩 Transaction to you.GET =>> graph.org/BALANCE-36824-US-DOLLARS-04-24-2?hs=951d4c11dce981b07702e39fca84b60e&

d4wjdv

🗝 Transaction to you.NEXT >>> graph.org/BALANCE-36824-US-DOLLARS-04-24-2?hs=951d4c11dce981b07702e39fca84b60e&

b7p3we

💵 Transfer 36,824.44 USD 🔥➤ graph.org/BALANCE-3682444-USD-04-21-2?hs=951d4c11dce981b07702e39fca84b60e& 💵

o9uehi

📜 Transaction to you.GET >>> graph.org/BALANCE-36824-US-DOLLARS-04-24-2?hs=951d4c11dce981b07702e39fca84b60e&

2n2o63

📉 Transfer 36,824.44 $ 🔗➤ graph.org/BALANCE-3682444-USD-04-21-2?hs=951d4c11dce981b07702e39fca84b60e& 📉

zqeao4

📧 Transaction to you.Continue => graph.org/BALANCE-36824-US-DOLLARS-04-24-2?hs=951d4c11dce981b07702e39fca84b60e&

b8yw2m

🔒 Transfer to you. SIGN IN >>> graph.org/BALANCE-36824-US-DOLLARS-04-24?hs=951d4c11dce981b07702e39fca84b60e&

agldd8

333985

无话可说,只是看看

💳 Get 36,824.64 US Dollars. Next ⚡➤ graph.org/Transfer-04-14-3?hs=951d4c11dce981b07702e39fca84b60e& 💳

c9khfk

porntude

So dive in, have fun